The 20% QBI Deduction Is Now Permanent. Here's the Honest Breakdown for Freelancers.

The QBI deduction is now permanent. Learn who qualifies, what the OBBBA actually changed in 2026, and how Form 8995 connects the deduction to your return.

Every year, tax software asks whether you have "qualified business income." Most self-employed filers answer yes and move on without fully understanding what they just claimed. The deduction it refers to is worth 20% of that income. And as of 2026, it no longer expires.

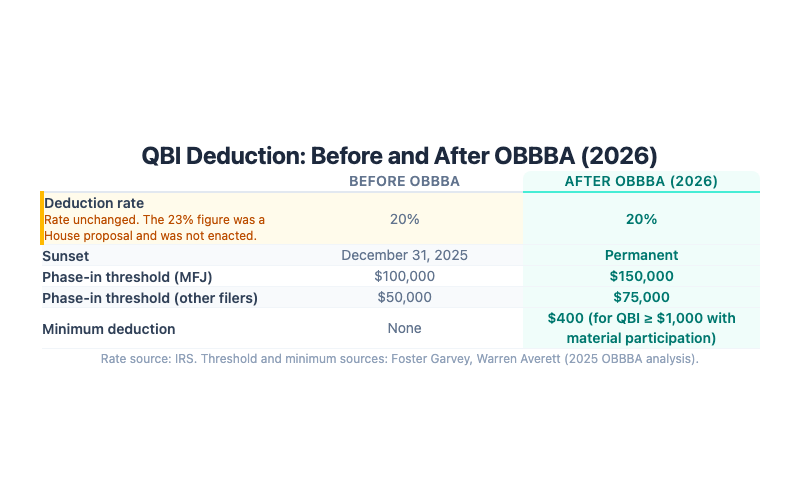

The One Big Beautiful Bill Act, signed July 4, 2025, made the Section 199A qualified business income deduction permanent. [1] Before that, it was scheduled to sunset after 2025. The law also raised the income thresholds at which the deduction starts to phase in, and added a $400 guaranteed minimum for filers with at least $1,000 of qualifying income. [3]

One thing the law did not change: the rate stayed at 20%. Some coverage of the OBBBA states the rate rose to 23%. That figure comes from an earlier House-passed version of the bill. It was not enacted. The IRS rate is 20%, and the enacted law kept it there. [1] [2]

This post covers what qualified business income is, which entity types qualify, what OBBBA actually changed and what it did not, how the deduction is calculated with plain numbers, and how Form 8995 connects the deduction to your return. If you file Schedule C, this deduction almost certainly applies to you.

What "qualified business income" actually means

The IRS defines qualified business income as "the net amount of qualified items of income, gain, deduction, and loss from any qualified trade or business." [5]

Two words in that definition matter: net and qualified.

Net means the deduction is calculated on what is left after deductible business expenses, not on your gross receipts. If you invoice $80,000 and deduct $20,000 in legitimate business expenses, your QBI is $60,000, not $80,000.

Qualified means not every category of income counts. The following are excluded from QBI:

- Capital gains and losses

- Dividends and interest income

- Income from wages (W-2 employment income from a separate employer)

- Income not connected to a qualified trade or business

The deduction applies to what is left: net income from a trade or business you operate. For most Schedule C filers, that is the profit line on Schedule C. Deductions that reduce your Schedule C net income, such as a home office deduction or business mileage, proportionally reduce the QBI figure the deduction is calculated from.

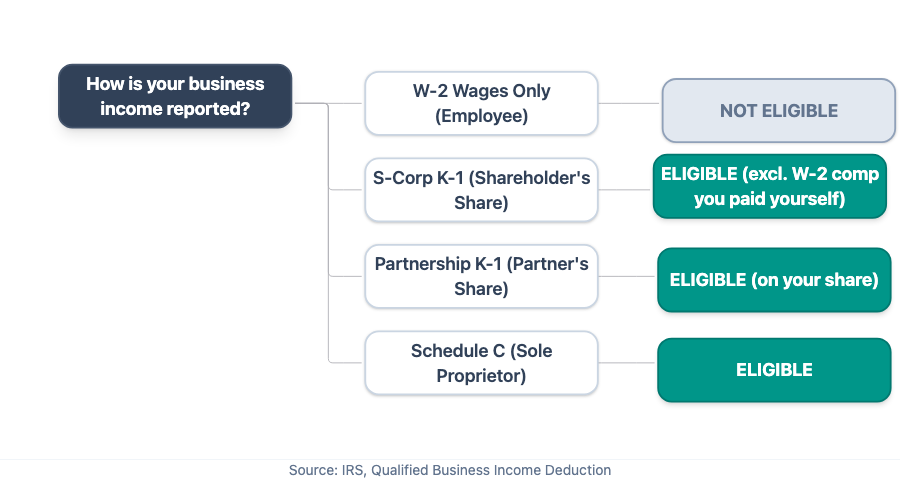

Who qualifies for the QBI deduction

The deduction is available to individual owners of pass-through entities: businesses whose income flows through to the owner's Form 1040 rather than being taxed at the entity level. [5]

Sole proprietors (Schedule C). If you are self-employed and file Schedule C, your net profit from self-employment is QBI. This includes freelancers, consultants, independent contractors, and single-owner businesses.

Sole-member LLCs. A single-member LLC is treated as a sole proprietorship for federal tax purposes by default. Income goes on Schedule C, and that income qualifies.

Partners with self-employment income. If you are a partner in a partnership, your allocable share of the partnership's qualified business income flows to your Form 1040 as QBI. Multi-member LLCs taxed as partnerships follow the same rule.

S-corporation shareholders. Your share of an S-corporation's qualified business income counts. One important nuance: the reasonable W-2 compensation you pay yourself as an S-corp shareholder is excluded from QBI. That salary is wage income, not business income, and wages are carved out of the definition.

What does not qualify. Income from performing services as an employee, investment income, and income from certain "specified service trades or businesses" above income thresholds (law, accounting, consulting, health, financial services, and similar fields at higher income levels) may be limited or excluded. If you are above the phase-in thresholds in a specified service business, that adds complexity; the simplified rules here apply to most Schedule C filers below those thresholds.

The deduction belongs on the individual return, not the business entity's return. It reduces your personal taxable income on Form 1040.

The next question is what the OBBBA actually changed in 2026, and what, despite some coverage, it did not.

What the OBBBA changed in 2026, and what it didn't

The One Big Beautiful Bill Act (H.R. 1) was signed July 4, 2025. The QBI changes take effect for tax year 2026; nothing changed for 2025 returns. [3]

What changed:

The deduction is now permanent. Section 199A had a built-in expiration after December 31, 2025. That sunset was removed. If you are planning your business finances beyond 2025, the deduction is part of the permanent tax landscape. [1] [4]

The phase-in thresholds increased. Before OBBBA, the deduction started to phase in (and the calculation got more complex) once taxable income exceeded $100,000 for married filing jointly, or $50,000 for all other filers. Starting in 2026, those thresholds are $150,000 for married filing jointly and $75,000 for all other filers. [2] [3] Below those amounts, the deduction is a straightforward 20% of net QBI.

A $400 minimum deduction was added. New Code Sec. 199A(i) guarantees a $400 deduction for any taxpayer with at least $1,000 of QBI from a qualified trade or business in which they materially participate (within the meaning of IRC §469(h)). Both the $400 minimum and the $1,000 QBI floor are indexed for inflation after 2026. [1] [3]

What did not change:

The rate stayed at 20%. Earlier versions of the bill included a proposal to raise the rate to 23%. That version passed the House. It did not survive into the final law. The IRS rate is 20%, and the OBBBA kept it there. [1] [2]

Some online sources, including a prominent self-employed explainer, state the rate rose to 23%. That figure is from the House version of H.R. 1. It is not the law. If you are using 23% to estimate your deduction, adjust that number down.

How the deduction is calculated: a plain-numbers example

For filers below the phase-in thresholds, the calculation is straightforward:

QBI deduction = 20% x net qualified business income

Take a freelance graphic designer with $80,000 in gross client billings. After deducting $20,000 in legitimate business expenses (home office, software subscriptions, equipment, mileage), their Schedule C net profit is $60,000. That $60,000 is their QBI.

Deduction: 20% x $60,000 = $12,000

That $12,000 reduces their taxable income. It is not a credit, and it does not appear as a refund. It works the same way any deduction does: it reduces the income the tax rate is applied to.

The $400 minimum applies when the calculated deduction would otherwise fall below $400. A part-time consultant with $1,500 of net QBI would calculate 20% x $1,500 = $300. Because $300 is below the $400 minimum, and they have at least $1,000 in QBI and materially participate in the business, the deduction is $400 instead of $300.

For filers above the phase-in thresholds ($150,000 MFJ, $75,000 other filers), the calculation adds W-2 wage and unadjusted property basis components. That complexity is beyond the scope of this post. If your taxable income puts you above those thresholds, Form 8995-A handles the additional computation, and a tax professional can walk through the specifics for your situation.

All numbers above are illustrative. The actual deduction for any individual depends on their specific income, expenses, filing status, and business type. The form that calculates this is Form 8995, and for most filers, it is a one-page worksheet.

How Form 8995 connects the deduction to your return

The QBI deduction is claimed on Form 8995 (Qualified Business Income Deduction Simplified Computation). [6] For most self-employed filers below the phase-in thresholds, Form 8995 is a one-page worksheet. It collects the QBI figures from your business activities, applies the 20% rate, factors in any limitations, and produces the deduction amount.

Form 8995-A is used for filers above the phase-in thresholds or those with more complex structures: multiple businesses, specified service trades, or significant W-2 wages and qualified property in the calculation. If Form 8995 applies to you, the computation is straightforward.

The deduction flows from Form 8995 to line 13 of Form 1040, reducing your taxable income. It is technically a "below-the-line" deduction, but it functions like an above-the-line deduction because it reduces taxable income regardless of whether you itemize or take the standard deduction.

Tax software populates Form 8995 automatically once you have entered your Schedule C income and expenses. The form itself is not where the work happens. The work happens on Schedule C, which is only as accurate as the business expense records behind it.

The IRS receipt documentation standards that govern your Schedule C deductions are the same standards that determine the net-income figure QBI is computed from. What you can substantiate as a deductible expense shapes the profit number Form 8995 works from. More on what those documentation standards actually require.

The records connection: why your Schedule C expenses shape the deduction

QBI is net business income. That means every deductible business expense that reduces your Schedule C profit also reduces the QBI the deduction is applied to.

That might sound like expenses hurt your deduction. They do, slightly. But the framing misses the point. Expenses reduce your taxable income by their full amount. The QBI deduction reduces taxable income by 20% of QBI. The net result of a legitimate business expense is almost always in your favor, even after accounting for the smaller QBI.

What records protect is not the deduction size. What they protect is the defensibility of the net-income number you reported.

Here is a practical version. A $3,000 mileage deduction reduces Schedule C net income from $63,000 to $60,000. The QBI deduction falls from 20% x $63,000 = $12,600 to 20% x $60,000 = $12,000. The mileage deduction cost $600 of QBI benefit. But it reduced taxable income by $3,000 directly, so the net benefit is $2,400 in deduction value (before the tax rate), not a loss.

The records matter because if the $3,000 mileage deduction is ever questioned, you need to substantiate it. The mileage log requirements that apply to Schedule C are the same rules that apply to the net income QBI is calculated from. A deduction you cannot prove is a deduction that gets disallowed, which raises your Schedule C profit, which raises your QBI, which raises your tax bill.

Organized, retrievable expense records are what make the Schedule C profit number defensible. Your QBI deduction is calculated from your net business income, and the records that prove your deductible expenses are what establish that number. ReceiptNote captures the vendor, amount, date, and category from a receipt photo and stores them as organized, retrievable digital records. It is free to get started.

TL;DR summary

| What | Detail |

|---|---|

| Who qualifies | Sole proprietors (Schedule C), partners with SE income, LLC members, S-corp shareholders (excluding W-2 comp paid to yourself) |

| Rate | 20% of net QBI. The 23% figure in some sources was a House proposal; the enacted law kept 20% |

| New in 2026 | Deduction made permanent; phase-in thresholds raised to $150,000 MFJ / $75,000 other filers; $400 minimum for QBI of at least $1,000 with material participation |

| Phase-in applies when | Taxable income is above $150,000 (MFJ) or $75,000 (other filers) |

| What it is not | An income tax credit; it does not show up as a refund; it reduces taxable income |

| Form | Form 8995 (most filers); Form 8995-A (higher earners or more complex structures) |

| Records matter because | QBI is net business income; the deduction is calculated from your Schedule C profit, which your expense records establish |

The QBI deduction has been in the code since 2018. For eight years it carried an expiration date. It no longer does. If you file Schedule C, your net business income qualifies. The calculation is a single form for most filers. And the same discipline that makes your Schedule C defensible is what makes the deduction defensible too.

If you want a starting point for the expense record side of that equation, ReceiptNote keeps those records organized and retrievable from the moment you photograph a receipt.

These are federal rules as published by the IRS and reflected in independent legal and CPA analysis. This is general information, not tax advice. Your specific situation may involve factors that change how the rules apply to you. A tax professional can work through that.

References

- Foster Garvey, "Larry's Tax Law -- One Big Beautiful Bill Act Part 4: Qualified Business Income Deduction, Code Section 199A" https://www.foster.com/larry-s-tax-law/one-big-beautiful-bill-act-part-4-qualified-business-income-deduction-code-section-199a

- Tax Foundation, "199A Deduction: Pass-Through Business Deduction and the Big Beautiful Bill" https://taxfoundation.org/blog/199a-deduction-pass-through-business-big-beautiful-bill/

- Warren Averett, "OBBBA Breakdown: Qualified Business Income (QBI) Deduction" https://warrenaverett.com/insights/one-big-beautiful-bill-breakdown-qualified-business-income/

- RSM US, "Permanent QBI deduction provides some tax planning certainty" https://rsmus.com/insights/services/business-tax/obbba-tax-qbi-deduction.html

- IRS, "Qualified Business Income Deduction" https://www.irs.gov/newsroom/qualified-business-income-deduction

- IRS, "About Form 8995, Qualified Business Income Deduction Simplified Computation" https://www.irs.gov/forms-pubs/about-form-8995