How Self-Employed Drivers Can Protect a $7,000+ Mileage Deduction at Audit

The 2026 IRS mileage rate is 72.5 cents per mile. Most self-employed filers focus on that number and skip the records standard that determines whether they actually keep the deduction. Here is what the IRS requires, and what fails at audit.

The IRS set the 2026 standard mileage rate at 72.5 cents per mile, up 2.5 cents from 2025. [1] Every January that number gets a lot of attention from self-employed people who drive for work.

The rate is the easy part.

The harder question is whether your records meet the IRS mileage log requirements, the standard that determines whether the deduction holds up if that return is ever reviewed. Most logs do not. Not because people are dishonest, but because the recordkeeping requirement is more specific than "write down your miles." The IRS requires five fields per trip entry, built at or near the time of travel. A log that is missing a field, or was reconstructed from memory at year-end, is a log that can be partially or fully disallowed. [2]

This post covers who qualifies, what each log entry must contain, what "contemporaneous" means in practice, what happens when a log fails, and one method election that cannot be undone once a vehicle enters business use.

Who this deduction is for, and which trips actually qualify

As of 2026, the business mileage deduction is exclusively for self-employed filers. W-2 employees permanently lost the unreimbursed employee mileage deduction under the One Big Beautiful Bill Act. [3] If you file a Schedule C as a sole proprietor or single-member LLC, this deduction applies to you. If you receive only a W-2, it does not.

The trips that count: [3]

- Driving between two business locations, for example from your office to a client site

- Driving from home to a temporary worksite

- Driving to meet clients or customers

- Business errands such as picking up supplies or making a bank deposit

What does not count: the daily commute from home to a regular, fixed office. That trip is personal travel. The exception applies when your home is your principal place of business. If you have a qualifying home office and drive from it to a client meeting, that trip is deductible.

The fastest way to inflate and then lose a mileage deduction is claiming regular commute miles. Identify those trips as personal before they go in the log.

Once you know which trips belong, the next question is what each entry must contain.

What the IRS requires in every mileage log entry

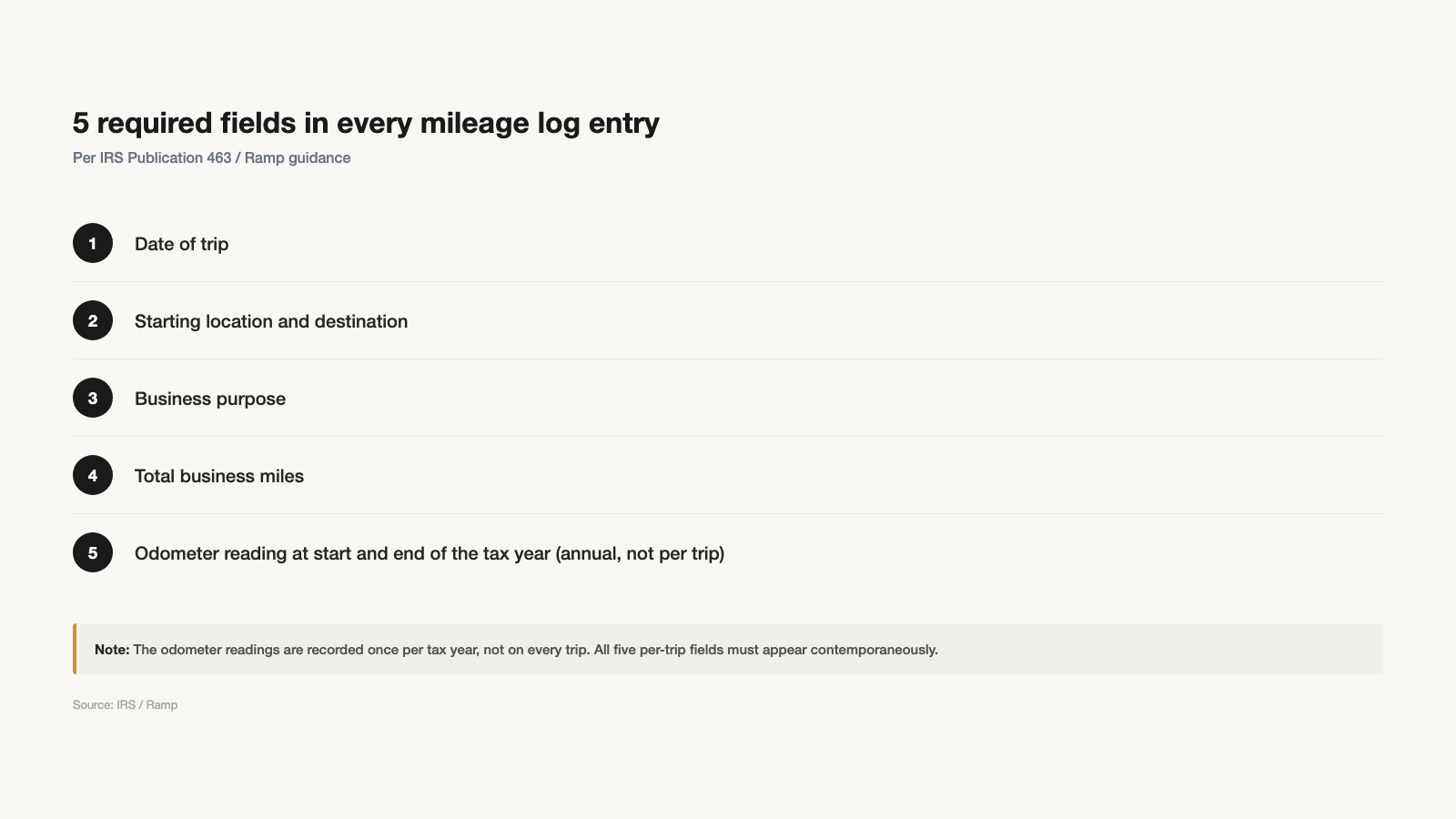

A mileage log has a specific required structure. Each trip entry must contain five elements: [2]

- Date of the trip.

- Starting location and destination.

- Business purpose for the trip.

- Total business miles for the trip.

- Odometer readings at the start and end of the tax year (not per trip, but once for the full year).

That fifth element is the one most often missing. Without the year-start and year-end odometer readings, the IRS cannot verify the business-to-total-miles ratio used to compute the deduction.

No prescribed format exists. A spreadsheet, a notebook, a mileage app: any of these work as long as all five fields appear in every entry. The format is less important than the completeness and timing of each record.

Completeness covers what to write. Timing is the other half of the standard.

What "contemporaneous" means, and why reconstruction is risky

"Contemporaneous" is the IRS word for records that meet the timing standard. It means the record was created at or near the time the travel occurred, not compiled months later during tax preparation. [2]

In practice, the IRS considers a mileage log timely if it is updated weekly. [3] That means logging each trip the same day, or catching up before the week closes. Waiting until tax season to reconstruct a year of driving from memory or from a navigation app's history does not meet that standard.

Two things to understand about reconstruction:

Reconstructed logs are not automatically disqualified. [2] Corroborating evidence (calendar entries, client invoices, appointment confirmations, emails) can support a reconstructed record. The IRS does accept reconstructed logs in some circumstances.

But they carry materially higher risk. Even with supporting evidence, a reconstructed log is more exposed to challenge than one built in real time. [2] Year-end reconstruction from a navigation app's history is the weakest defensible position: it is both reconstructed rather than contemporaneous, and unlikely to satisfy the weekly-timeliness bar. (That is a judgment drawn from combining sources [2] and [3], not a direct IRS statement.) It is not automatically rejected. It is simply the record most likely to face a question it cannot answer.

The discipline maps directly to the habit of capturing receipts at the moment of an expense. The capture at the time, not later principle covers mileage entries and expense receipts for the same reason: a record built at the time is easier to defend than one rebuilt afterward.

The stakes of getting this wrong are concrete. At 72.5 cents per mile, they add up quickly.

What disallowance actually looks like, and how much is at risk

When the IRS determines that a mileage log does not meet the required standard, it can disallow some or all of the deduction claimed, and may assess interest on any resulting underpayment. [2]

The dollar exposure scales with how much you drive. At 72.5 cents per mile, a 10,000-business-mile year is a $7,250 deduction. [1] That is illustrative arithmetic based on the IRS rate; your number depends on your documented miles. The point is the scale: a disallowed log does not produce a minor bookkeeping penalty. It removes the deduction.

There is a compounding factor. Mileage deductions reduce Schedule C net profit. Because self-employment tax is computed on net profit, a disallowed deduction hits income tax and self-employment tax simultaneously. [3] At typical combined effective rates for self-employed filers, a $7,250 disallowance can translate to $1,500 to $2,000 or more in additional tax, before interest. (That figure is illustrative; the actual impact depends on your bracket, deductions, and filing situation.)

This is not meant to induce alarm about paperwork. The cost of disallowance is just the concrete case for keeping the log current. The work involved in logging a trip takes less time than the trip itself.

Before you can protect the deduction, you need to make one decision that follows a vehicle for its entire business life.

Standard mileage vs actual expenses: the decision that does not reverse

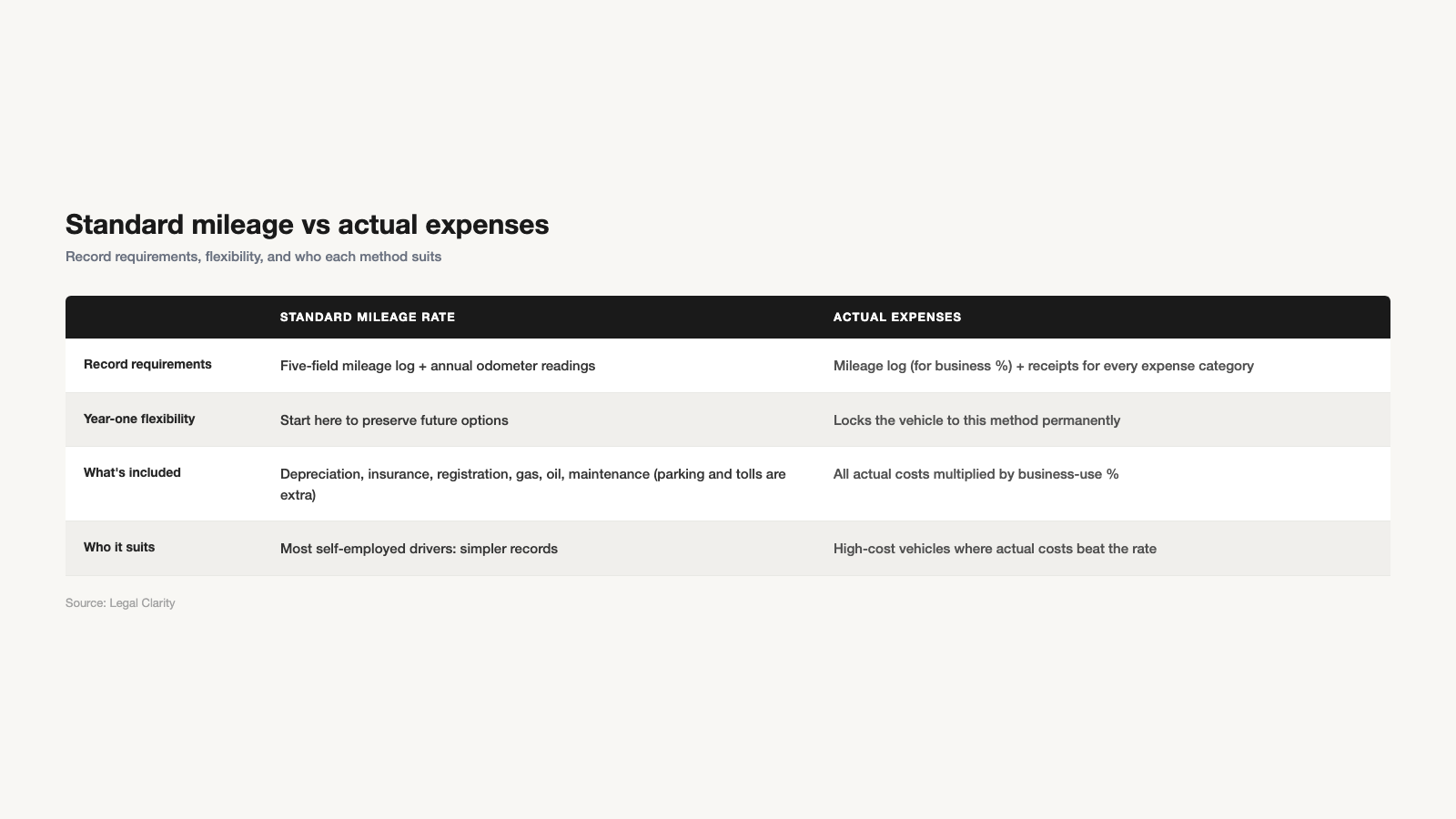

Before you drive the first business mile in a vehicle, you need to choose a method. That choice has consequences that extend for the life of the car.

Standard mileage rate. Multiply the IRS rate (72.5 cents in 2026 [1]) by your documented business miles. The rate already accounts for depreciation, insurance, registration, gas, oil, and maintenance. Parking fees and tolls are deductible separately on top of the rate. [4] The record requirement is the five-field mileage log.

Actual expense method. Deduct the real operating costs: gas, repairs, insurance, registration, depreciation or lease payments, multiplied by the percentage of miles used for business. This requires receipts for each expense category, plus a mileage log to establish the business-use percentage. [4]

The asymmetry matters: if you start with actual expenses in a vehicle's first year of business use, that vehicle is locked into actual expenses permanently. You cannot switch to the standard mileage rate for that vehicle in a future year. [4]

If you start with standard mileage instead, you retain flexibility. For vehicles you own, you can switch to actual expenses in a later year (though the reverse switch is not available). Leased vehicles must keep standard mileage for the full lease period if that is the method elected at the outset. [4]

The one-way door on actual expenses is the most consequential, least-known fact in vehicle deductions. Choosing actual expenses in a high-cost first year can make financial sense if you have compared the two methods for your specific situation. Defaulting to actual expenses without that comparison forecloses future flexibility for that vehicle with no way back. (That is a judgment drawn from the lock-in rule in source [4], not an IRS recommendation on which method to choose. A tax professional can run the comparison for your numbers.)

Whichever method you use for a given vehicle, the log requirement is the same. Both methods sit inside the same Schedule C paper trail as your other expense records.

Mileage records and the Schedule C paper trail

Mileage logs and receipt records are parallel substantiation regimes. Both require contemporaneous documentation. Both feed Schedule C. Both sit under the same burden-of-proof standard: you claimed the deduction, you provide the evidence.

The practical upshot is that the record habits reinforce each other. The discipline of logging a trip before the week closes is the same discipline that goes into capturing a receipt at the time of an expense. A self-employed person who already keeps receipts contemporaneously has the muscle memory. Applying it to mileage keeps both records defensible under the same standard.

The five elements that govern receipt substantiation (amount, date, place, business purpose, business relationship) are the subject of the same substantiation standard that governs your receipt records. Mileage logs are the vehicle-expense parallel of that standard.

Both feed into the broader self-employed paper trail: mileage deductions reduce Schedule C net profit, which affects both income tax and self-employment tax. A complete paper trail covers both.

The deduction survives or fails based on what the record shows, and when it was written.

Keeping the log means keeping the deduction

The 2026 IRS mileage rate is 72.5 cents per mile. [1] That number is the part that gets announced. The mileage log requirements determine whether you leave the deduction intact.

Five fields per trip entry. Updated within the week. Odometer readings at the start and end of the year. Method election made before the first business trip in a new vehicle's life.

That is the complete standard. A log built on those terms is a log that can answer the question.

The contemporaneous discipline that keeps a mileage log defensible is the same habit as capturing a receipt at the moment of the expense. ReceiptNote captures the receipt fields that belong in the same Schedule C paper trail as your mileage log, kept in one place so both records stay current.

Start your free paper trail. Download ReceiptNote.

Quick-reference summary

| Topic | What to know |

|---|---|

| 2026 standard mileage rate | 72.5 cents per mile (up from 70 cents in 2025) [1] |

| Who qualifies | Self-employed Schedule C filers only; W-2 employees ineligible as of 2026 [3] |

| Deductible trips | Client meetings, business errands, home-to-temporary-worksite, between two workplaces; regular commute excluded [3] |

| Five required log fields | Date, starting location and destination, business purpose, business miles, year-start and year-end odometer [2] |

| Timing standard | Updated weekly at minimum; year-end reconstruction is allowed but materially higher-risk [2] [3] |

| Disallowance risk | Inadequate records can result in partial or full disallowance of the deduction, plus interest [2] |

| Method election | Starting with actual expenses locks that vehicle into that method permanently; standard mileage preserves flexibility for owned vehicles [4] |

References

- IRS: IRS sets 2026 business standard mileage rate at 72.5 cents per mile https://www.irs.gov/newsroom/irs-sets-2026-business-standard-mileage-rate-at-725-cents-per-mile-up-25-cents

- Ramp: IRS mileage log requirements https://ramp.com/blog/irs-mileage-log-requirements

- Driversnote: IRS mileage guide, self-employed deductions https://www.driversnote.com/irs-mileage-guide/self-employed-deductions

- Legal Clarity: 2026 IRS standard mileage rates and deduction rules https://legalclarity.org/2026-irs-standard-mileage-rates-and-deduction-rules/