Home Office Deduction for the Self-Employed: The Two Tests That Decide Your Claim

Most home office deductions that fail at audit fail on one test: exclusive use. Here is what the IRS actually requires from self-employed filers, how both calculation methods work, and what records you need to keep.

The home office deduction has a reputation for being risky. The real risk isn't claiming it. It's claiming it wrong.

The IRS doesn't treat the home office deduction as a red flag on its own. What draws scrutiny is a claim that can't be supported when someone looks at the records.

If you're self-employed and you work from a dedicated space at home, the deduction is available. IRS Publication 587 and Topic No. 509 describe exactly what qualifies and what doesn't. [1] [2] This post covers the eligibility tests, both calculation methods, and the records the IRS expects from a home office claim.

Who qualifies for the home office deduction

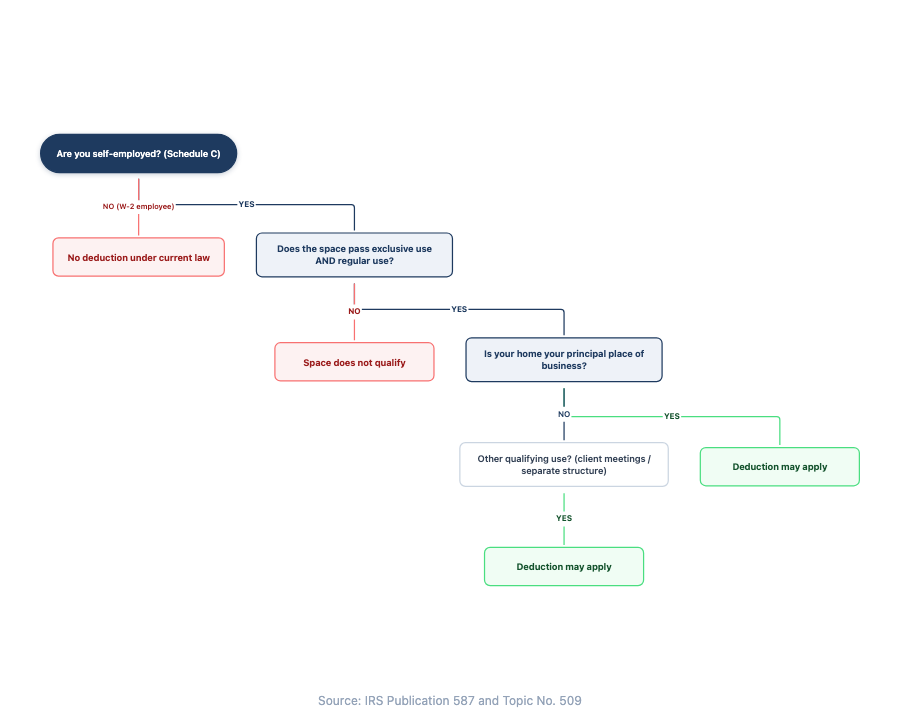

W-2 employees working from home do not qualify for the home office deduction. IRS Publication 587 includes a decision flowchart: if you're using a space "as an employee," the flowchart closes with "No deduction." [2] The Tax Cuts and Jobs Act of 2017 suspended the miscellaneous itemized deduction that previously allowed employees to claim unreimbursed work expenses; under that law, the suspension runs through tax year 2025. W-2 remote workers aren't eligible under current law regardless of how much of their home is set aside for work.

The rest of this post is for self-employed people: sole proprietors, freelancers, consultants, and single-member LLC owners who file Schedule C.

Two other situations also qualify but are narrower in scope. Partners using part of their home for partnership business and certain home day care providers may qualify under separate provisions of Pub 587. Those scenarios have their own rules and aren't covered here. The qualifying tests that follow apply to Schedule C self-employed filers.

The two tests your workspace must pass

Both tests must be met. Passing one and failing the other means the deduction doesn't apply.

Test 1: Exclusive use. IRS Publication 587 defines this precisely: the space must be "a specific area of your home only for your trade or business." [2] The word "only" carries most of the weight. A space used for business during the day and as a guest room on weekends doesn't qualify. A space used for work but also storing personal belongings, hosting family video calls, or serving as a homework area doesn't qualify either.

The IRS's own example makes the rule concrete. An attorney uses a den at home to prepare legal briefs. The attorney's family also uses the den for recreation. The IRS says: the den is not used exclusively in the attorney's trade or business, so no deduction applies. [2] The attorney works there every day, but that doesn't matter. Mixed use cancels the claim.

The space doesn't have to be a separate room. A clearly delineated section of a room can qualify if it's used exclusively for business and nothing else occupies it. What the IRS is looking at is whether personal use can be shown for any part of the area being claimed.

Test 2: Regular use. The space must also be used on a regular basis for business, not just occasionally. The IRS doesn't set a minimum number of hours, but incidental use doesn't meet the standard.

The principal-place-of-business requirement. Beyond the two use tests, the home must also be your principal place of business. IRS Topic No. 509 includes a useful expansion here: a home qualifies when it's used for administrative or management activities (scheduling, billing, bookkeeping, client correspondence) and there is no other fixed location where you conduct those activities. [1] If your client work happens on-site but all your admin work happens at home, the home office can still qualify.

Other qualifying configurations include meeting clients at home in the normal course of business, or using a separate free-standing structure such as a studio or detached garage. If your workspace passes both tests, the next decision is how to calculate the deduction.

Two ways to calculate your deduction

Once your workspace qualifies, you choose between two calculation methods. The choice is made at filing, and the methods produce different results depending on your home costs and your business-use percentage.

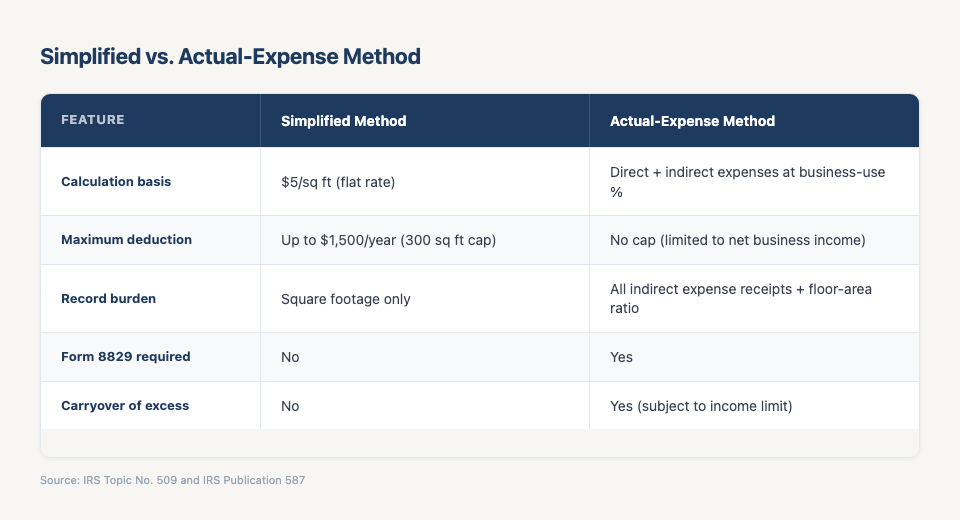

Simplified method. The IRS allows a flat rate of $5 per square foot, applied to a maximum of 300 square feet. The maximum deduction under this method is $1,500 per year. [1] No Form 8829 is needed. The deduction goes directly on Schedule C.

Actual-expense method. This method requires more work but often produces a larger deduction for filers with significant home costs.

Expenses divide into two categories. [2]

Direct expenses apply only to the business space itself: painting the office, repairing a window in that room, replacing flooring only in that area. These are fully deductible.

Indirect expenses cover the home as a whole: utility bills, rent (if you don't own the property), homeowner's or renter's insurance, general repairs, and depreciation. These are deductible at your business-use percentage, calculated as the square footage of your office divided by the total livable square footage of your home. If your home is 1,200 square feet and your office is 180 square feet, 15 percent of each indirect expense is deductible.

Under the actual-expense method, self-employed filers calculate the allowable amount on Form 8829 first, and the result transfers to Schedule C, Line 30. [1] [3]

Which method saves more depends on your square footage, your home costs, and your business-use percentage. Running the actual-expense numbers before committing to the simplified rate is worth doing. That's a question for your accountant or tax preparer. Whichever method you choose, the records that support your claim look the same.

The records you need to back up your claim

Documentation requirements differ by method, but in both cases the records exist before you file, not because of it.

For the simplified method, the key record is the square footage of your office. Measure the space and keep a note of the dimensions. If you're claiming a portion of a room rather than a full room, document exactly what area you're claiming and how you measured it.

For the actual-expense method, you need records for every indirect expense you're deducting at the business-use percentage: utility bills, rent or mortgage statements, insurance premiums, receipts for repairs that affect the whole home. For direct expenses, you need receipts for work done only in the office space. Each record should show the amount, date, and what it covered.

The IRS applies the same adequate-records standard to home office expenses that it applies to all business deductions. A record needs to show what was paid, when, and what it was for. A utility bill covers the first two. Your floor-area calculation and business-use percentage establish the rest.

Digital records qualify under Rev. Proc. 97-22 when they're legible and reproducible on request. A phone photo of a utility bill stored in a retrievable system works. A file buried in a camera roll that can't be produced clearly on request is harder to defend. The retention guidance in that same receipt documentation post covers how long these records need to survive.

If you're building the habit of capturing these records as they arrive rather than reconstructing them at filing time, the post on the four-stage paper trail for self-employed filers covers how that system works in practice. The last question most filers have is what an IRS examiner actually looks at when a home office claim is reviewed.

What the IRS actually examines

The home office deduction doesn't trigger an audit by itself. It's a legitimate Schedule C line item used by millions of self-employed filers.

What creates problems is inconsistency between what's claimed and what the records show. If you claim exclusive use but your documentation, photos, or expense records suggest the space had personal uses, that's the gap the IRS is looking at. Exclusive-use failure is where most home office claims break down in examination, because it's also where most filers are less rigorous than the rule requires. [2]

There's also an income limit worth knowing about. Under the actual-expense method, the home office deduction cannot exceed the net income your business generated. If your Schedule C shows a loss or very small net income, the deductible amount is capped accordingly. Form 8829 handles this calculation; amounts that exceed the cap in one year can carry forward under certain circumstances. [3]

The records that protect your claim are concrete: the floor area you measured, documentation that shows the space is dedicated to work, and the expense receipts that show what you paid to operate it. The IRS applies the same contemporaneous-records principle here that it applies to vehicle deductions. Records made near the time of the event carry more weight than those assembled from memory later.

The home office deduction has clear rules. Qualifying is binary: you either have exclusive use or you don't. The calculation methods are defined by the IRS and the forms that go with them. The records required are the same ones the IRS expects for any business expense, applied to your home costs.

What makes the actual-expense method more demanding isn't the math. It's the habit of keeping indirect-expense records throughout the year. Utility bills, insurance statements, repair receipts: these arrive at regular intervals and are easy to lose track of without a system. ReceiptNote captures vendor, amount, date, and category from a receipt photo and stores them as organized, retrievable digital records, the same standard that satisfies Rev. Proc. 97-22 for electronic storage.

Try ReceiptNote free: photograph your first expense receipt in under a minute.

These are federal rules as published by the IRS, not tax advice. Your specific situation may involve factors that affect how these rules apply to you. A tax professional can work through that.

TL;DR summary

| Topic | What to know |

|---|---|

| Who qualifies | Self-employed filers with a dedicated workspace at home; W-2 employees do not qualify under current law |

| Exclusive-use rule | The space must be used only for business; any personal use disqualifies the entire area being claimed |

| Calculation methods | Simplified: $5/sq ft, max 300 sq ft, up to $1,500/year; Actual: direct and indirect expenses calculated on Form 8829 |

| Key records | Simplified: floor area dimensions; Actual: utility bills, insurance, rent, and repair receipts for the whole home |

References

- IRS Topic No. 509, Business Use of Home https://www.irs.gov/taxtopics/tc509

- IRS Publication 587, Business Use of Your Home https://www.irs.gov/publications/p587

- IRS: About Form 8829, Expenses for Business Use of Your Home https://www.irs.gov/forms-pubs/about-form-8829