What IRS Receipt Requirements Mean for Your Records (and How Long to Keep Them)

The IRS does not ask whether you have a receipt. It asks what your record proves. Here is what business expense documentation must show, how long it must survive, and whether a phone photo counts.

Having a receipt is not the same as meeting IRS receipt requirements. The IRS does not ask whether you held on to the paper. It asks whether the record proves the expense was what you say it was.

Under the tax code, the burden of proof sits with the taxpayer. [2] You claim the deduction; you supply the evidence. A receipt that shows a total but not what was purchased, or what the business reason was, may not hold up if questions arise. Neither might a record you kept for only three years when your situation called for six.

This post maps the actual federal standards across four areas: what a record must show, how long it must survive, whether a phone photo qualifies, and how proof differs by expense type.

What "adequate records" actually means

The IRS uses the phrase "adequate records" but does not define it in one place. The governing logic is spread across several publications and guidance pages.

The starting point is Topic 305: you are required to keep records that support the income, deductions, and credits on your return, and those records must be available for IRS inspection. [6]

The burden-of-proof page is more direct: "The responsibility to prove entries, deductions, and statements made on your tax returns is known as the burden of proof. You must be able to prove (substantiate) certain elements of expenses to deduct them." [2] For most business expenses, that means documentary evidence: receipts, canceled checks, invoices, credit card slips.

One point worth marking early: proof of payment is not proof of deductibility. Publication 583 is clear that showing you paid for something does not, by itself, establish that the expense belongs on your tax return. [5] The record has to show both what you paid and why it was a legitimate business expense. That obligation is the thread running through the rules below, starting with what, exactly, a record must contain.

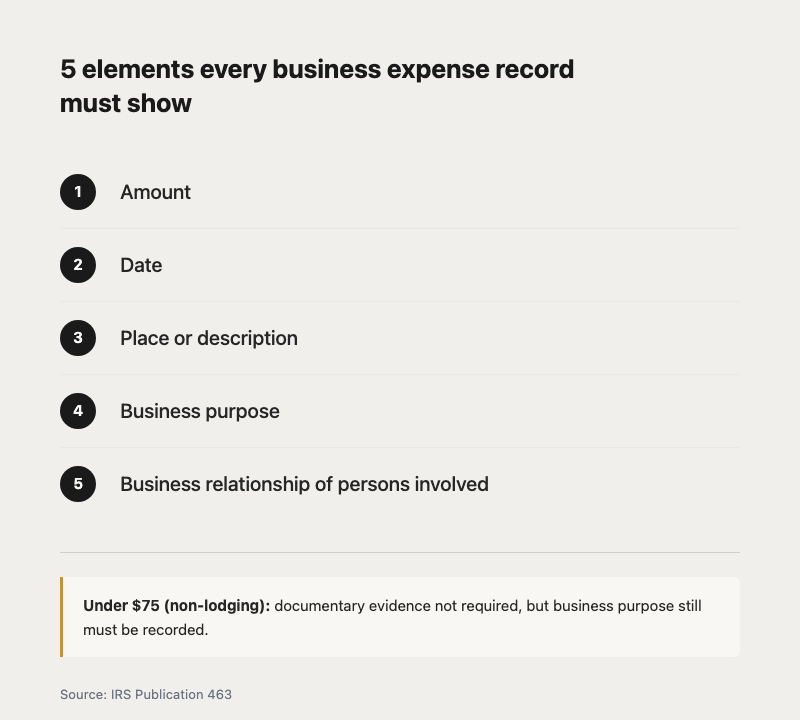

The five elements every business expense record must show

Publication 463 sets out what a business expense record must prove for travel, meals, and gifts. Five elements are required: [3]

- Amount: the total cost of the expense.

- Date: when the expense occurred.

- Place or description: where it took place, or a description of the item or service.

- Business purpose: the business reason for the expense, or the benefit you expected.

- Business relationship: for meals and entertainment, who you met with and their relationship to your business.

A receipt that shows only the total and the vendor satisfies elements one through three at best. Business purpose and business relationship are what most receipts do not capture on their own. That is the gap between possessing a receipt and having adequate substantiation.

Publication 463 also specifies that documentary evidence is "adequate" when it shows the amount, date, place, and essential character of the expense. [3] The phrase "essential character" means the record has to describe what the expense actually was, not just what it cost.

One exception applies. For non-lodging expenses under $75, documentary evidence is not required. [3] A $50 taxi, a $40 parking fee, a $65 business lunch: for these amounts, you do not need the receipt itself. Two things still apply, though: lodging always requires documentary evidence regardless of the amount, and the substantiation requirement does not disappear for sub-$75 expenses. You still need to record the business purpose. The exception covers only the documentary evidence requirement, not the underlying obligation to substantiate.

The five-element standard describes what a record must contain. The next question is how long that record has to survive, and the answer is not simply three years.

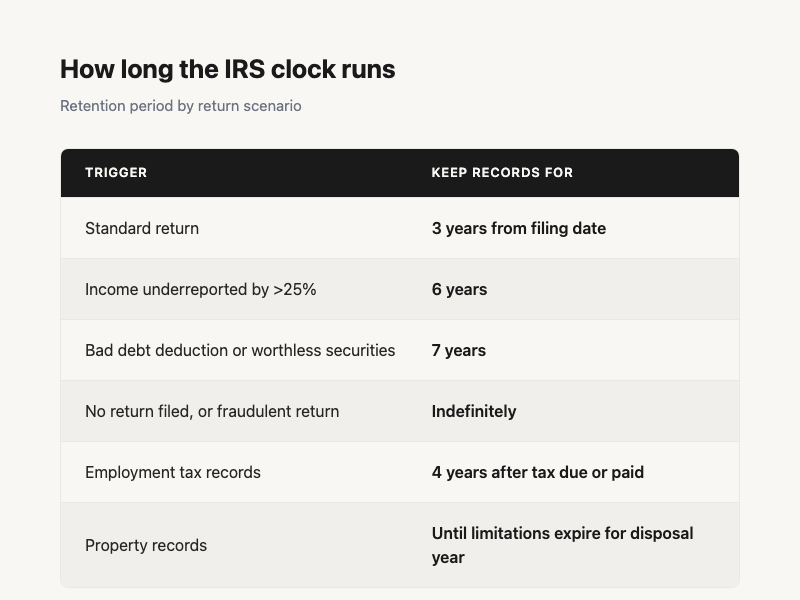

How long the IRS clock actually runs

The three-year rule is real, but it is the floor, not the ceiling. How long you need to keep records depends on what the IRS might examine and why.

The period of limitations is the window during which the IRS can assess additional tax. For most returns, that period is three years from the date you filed (or the due date, whichever is later). Records that support that return need to survive that window. [1]

Several situations extend or eliminate that window:

Two additional categories run on their own clock. Employment tax records (for businesses with employees) must be kept for at least four years after the date the tax was due or paid, whichever is later. [1] Property records work differently: keep them until the period of limitations expires for the year in which you disposed of the property. If you buy a piece of equipment in 2020, sell it in 2028, and the 2028 return is subject to a three-year window, the original purchase records need to survive until at least 2031.

The three-year rule applies cleanly to a standard, fully reported return with no major anomalies. Significant underreported income, a bad debt write-off, or a missed filing changes the timeline considerably.

With the retention question settled, the practical one that follows: does a phone photo satisfy the IRS, or does the record have to be on paper?

Do phone photos and scanned receipts count?

Yes, under specific conditions. The governing document is Revenue Procedure 97-22, published by the IRS in 1997 and still the controlling standard for electronic record storage. [4]

Under Rev. Proc. 97-22, records stored in a compliant electronic system satisfy IRC §6001, the code provision that requires records to be maintained. Three conditions apply.

First, the transfer from paper (or the original computerized records) to electronic format must be accurate and complete. Second, the system must be able to reproduce the records with "a high degree of legibility and readability" on screen and in hard copy when the IRS requests them. Third, the electronic storage system must function as the system of record. Once you have digitized documents under these conditions, you may discard the paper originals.

Publication 583 confirms this applies broadly: all requirements that govern hard-copy records apply equally to electronic storage systems. [5]

The practical meaning: a phone photo of a receipt stored in an organized digital system qualifies. A blurry scan in a folder of mixed files, one that cannot be reproduced legibly on request, does not automatically qualify, even though the file exists somewhere. Legibility and completeness are the conditions that make the format switch valid. The act of taking the photo is necessary but not sufficient on its own.

With the format question settled, the remaining one is whether the required elements differ depending on what type of expense is being documented.

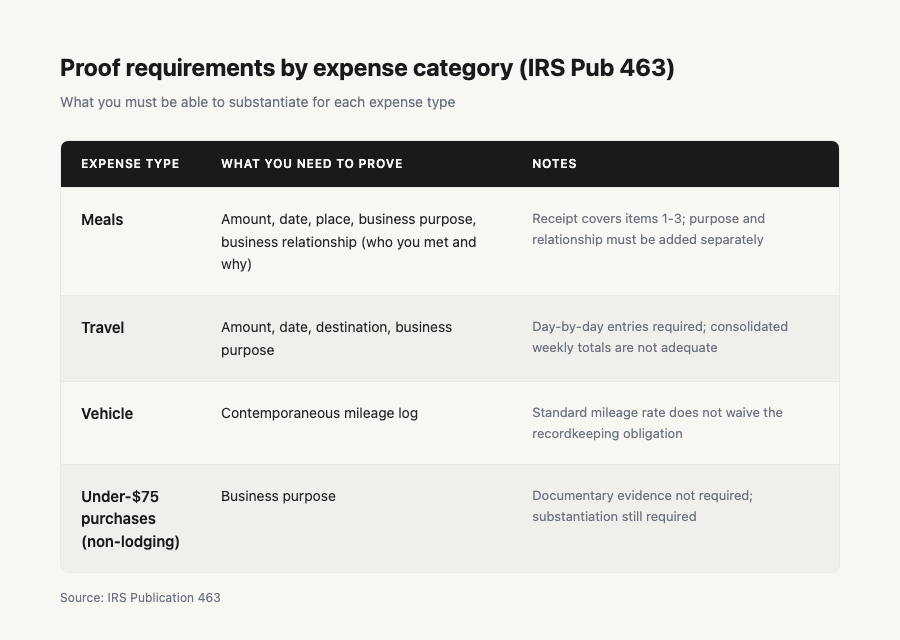

How IRS receipt requirements differ by expense category

The five elements apply across business expenses, but Publication 463 is explicit that travel, meals, gifts, and vehicle expenses carry specific documentation requirements. [3] Each behaves a little differently.

Meals. A business meal record needs all five elements: amount, date, place, business purpose, and business relationship (who you met with and why). The restaurant receipt typically covers the first three. The business purpose and the name and role of the other person come from a note you add at the time. Without them, the receipt handles only part of what is required.

Travel. For a business trip, documentation needs to show the amount, the date, the destination, and the business purpose. Day-by-day entries matter: consolidating a week of travel costs into one line without dates and destinations is not adequate documentation.

Vehicle. Whether you use the standard mileage rate or track actual expenses, you need contemporaneous mileage logs. The rate does not waive the recordkeeping obligation. Publication 463 notes that records made at or near the time of the expense carry more weight than reconstructed ones. [3] A log rebuilt from calendar entries in April is a weaker record than one maintained as you drove.

Under-$75 non-lodging expenses. The documentary evidence requirement does not apply to these, but the substantiation requirement does. The business purpose still needs to be recorded. The waiver covers the receipt; it does not cover the note explaining why the expense was a business deduction.

The records hold up when they cover the right elements for the right expense type. The last common gap is a different one: assuming a bank or card statement fills in whatever the receipt leaves out.

Why a card statement is not enough on its own

A credit card or bank statement shows you paid. It does not show what you paid for in business terms, or why the expense qualifies as a deduction.

Publication 583 is direct on this: proof of payment of an expense is not necessarily proof of the expense itself. [5] A statement might show "Restaurant $82" on a Friday in March. The IRS wants to know who you met with and what the meeting was about. The statement cannot supply that.

Timing matters here too. Publication 463 notes that contemporaneous records (made at or near the time of the expense) carry more weight than records reconstructed from memory later. [3] A note added while you are still at the table costs ten seconds. The same information, assembled from a calendar or vague recollection six months later, is an estimate.

This is where the behavioral side of receipt management connects to the rules. If you want the habit that makes meeting these documentation standards routine rather than a scramble, the companion post on five scanning habits that make meeting these rules easier day to day covers the operational side: when to capture, how to categorize, and how to add notes at the moment they are accurate.

Four rules, not one. A business receipt is adequate when it shows all five required elements. Records survive long enough when you understand which retention period applies to your situation. Digital storage qualifies when the system reproduces records legibly and completely. Category-specific proof matters because meals, travel, and vehicle expenses each require more than a total and a date. Together, this is what IRS receipt requirements demand from any record you intend to claim as a deduction.

These are federal rules as published by the IRS, not tax advice. Your specific situation may involve factors that change how the rules apply to you. A tax professional can work through that.

If the documentation side is where you want to start, ReceiptNote captures vendor, amount, date, and category from a receipt photo and gives you a note field for business purpose, the fields that map to adequate documentary evidence, kept together in one place.

Start capturing the fields that matter. Download ReceiptNote.

Quick-reference summary

| Rule area | What it requires |

|---|---|

| Documentary evidence | Amount, date, place, business purpose, business relationship (all five elements) |

| Retention period | 3 years (standard); 6 years if income underreported >25%; 7 years for bad debt; indefinite if no return filed |

| Digital records | Phone photos and scans qualify under Rev. Proc. 97-22 if legible and reproducible |

| Category differences | Meals and travel need all five elements; under-$75 non-lodging expenses waive the documentary-evidence requirement only |

| Payment proof | A card statement shows you paid; it does not show why the expense was a business deduction |

References

- IRS: How long should I keep records? https://www.irs.gov/businesses/small-businesses-self-employed/how-long-should-i-keep-records

- IRS: Burden of Proof https://www.irs.gov/businesses/small-businesses-self-employed/burden-of-proof

- IRS: Publication 463 (2025), Travel, Gift, and Car Expenses https://www.irs.gov/publications/p463

- IRS: Rev. Proc. 97-22, Electronic storage systems https://www.irs.gov/pub/irs-tege/rp-97-22.pdf

- IRS: Publication 583 (12/2024), Starting a Business and Keeping Records https://www.irs.gov/publications/p583

- IRS: Topic no. 305, Recordkeeping https://www.irs.gov/taxtopics/tc305