The 2026 Tax Breaks Freelancers Cheered, and the Ones They Actually Get

The biggest 2026 OBBBA tax breaks got a lot of attention. Most do not reach Schedule C filers. Here is a clear breakdown of which ones do, which are conditional, and which skip the self-employed entirely.

The 2026 tax breaks for freelancers got major coverage. When the One Big Beautiful Bill Act passed, the headlines were hard to miss. "No tax on tips." "No tax on overtime." A flood of coverage aimed at "working Americans." If you file a Schedule C and pay self-employment tax, you had good reason to pay attention. Some of those provisions do reach the self-employed. A few of the loudest ones do not.

The confusion is understandable. IRS guidance on each provision is split across separate pages. Coverage aimed at general audiences often does not sort by income type. And the phrase "working Americans" does not cleanly distinguish between employees who receive a W-2 and self-employed workers who file Schedule C. [1]

This post goes break by break, using IRS language, to give Schedule C filers a clear verdict on each.

Why the 2026 OBBBA headlines left freelancers with more questions than answers

The OBBBA introduced several new deductions. Some apply to all taxpayers. Some apply to employees specifically. Some apply to self-employed workers conditionally. And one provision that got heavy coverage applies exclusively to employees with overtime reported on a wage statement.

The problem is that coverage rarely labels which category a provision belongs to. A headline that says "no tax on overtime" does not specify that overtime, as a legal concept under the Fair Labor Standards Act, applies to nonexempt employees, not independent contractors or sole proprietors. A freelancer reading that headline has no clear signal that the provision was never written for them.

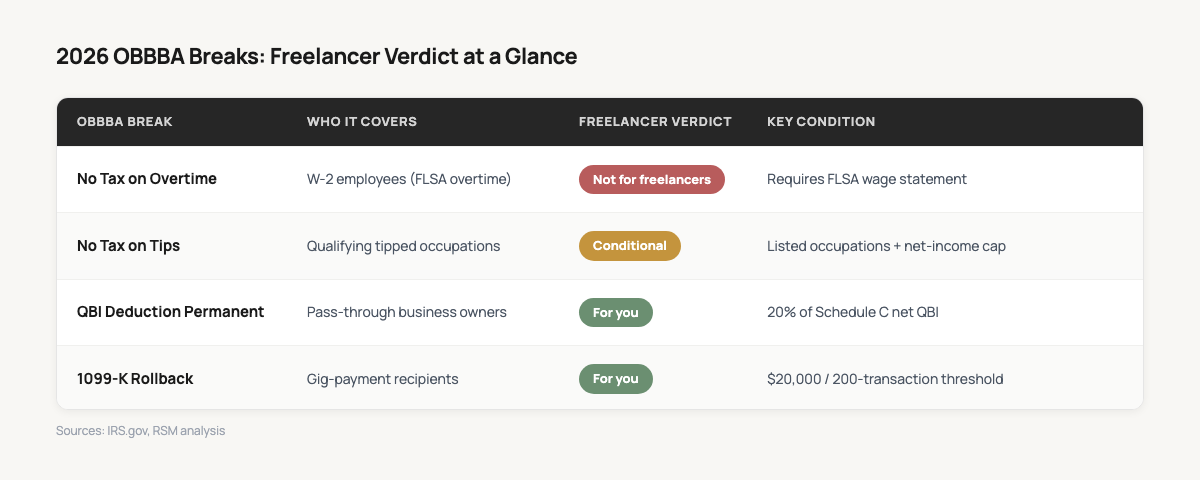

Before walking through each break, here is the at-a-glance summary. The detail follows.

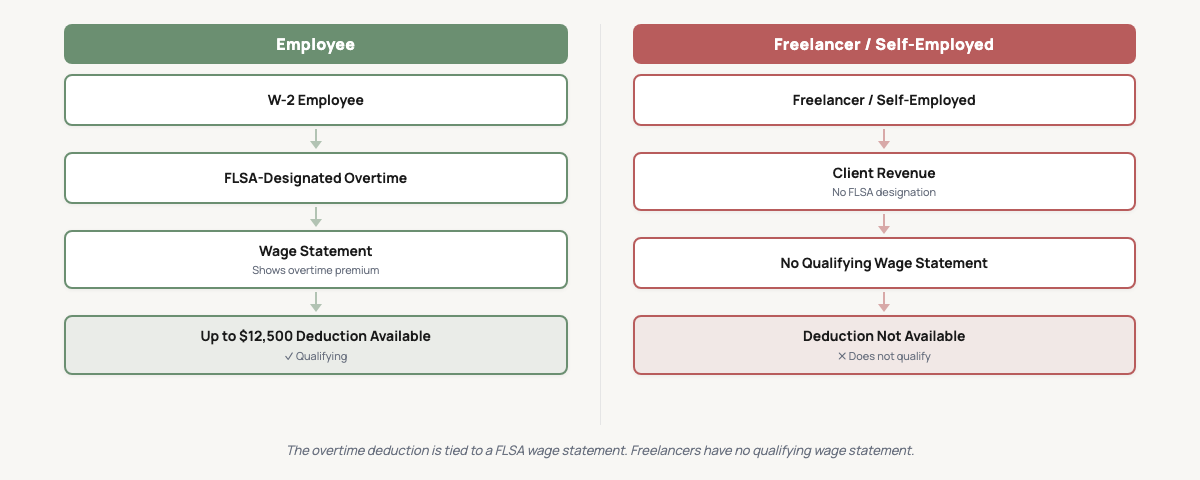

No tax on overtime: the provision that does not reach the self-employed

Verdict: Not for freelancers

The no-tax-on-overtime deduction is new for 2026. It covers up to $12,500 for single filers ($25,000 married filing jointly), with a MAGI phaseout above $150,000 single ($300,000 joint). It received heavy attention in coverage aimed at workers.

Here is the structural problem for freelancers: the deduction is tied to overtime as defined by the Fair Labor Standards Act. The FLSA covers nonexempt employees. It does not apply to independent contractors or self-employed workers. The deductible amount is specifically the premium portion of time-and-a-half overtime that is separately reported on a wage statement. [2]

Self-employed workers have no wage statement. They have no FLSA-designated overtime. There is no equivalent mechanism on Schedule C. The deduction was written for employees with overtime income.

From the IRS: "the FLSA overtime requirement does not apply to self-employed individuals." [2]

If you invoice a client for 60-hour weeks, that income appears as gross receipts on your Schedule C. It is not overtime in the FLSA sense. The deduction does not apply to it.

This is the single largest expectation gap in the 2026 OBBBA coverage for freelancers. It is worth naming clearly because the provision was framed as a "working Americans" benefit. Self-employed workers are working Americans. They are not employees under FLSA, and no workaround changes that. [1]

No tax on tips: real, but conditional for most freelancers

Verdict: Conditional

The no-tax-on-tips deduction does extend to self-employed individuals. That is a meaningful difference from the overtime provision. The deduction covers up to $25,000 in qualified tips, with a MAGI phaseout above $150,000 single ($300,000 joint). [1]

Two conditions narrow it sharply for most freelancers.

First: you must be in a qualifying occupation. The IRS and Treasury finalized regulations listing more than 70 specific occupations where workers customarily and regularly receive tips. [3] These are primarily food service, hospitality, and personal care roles: servers, bartenders, barbers, salon workers, hotel staff, parking attendants, and similar positions. Consultants, graphic designers, software developers, and writers are not on that list.

Second: for self-employed filers, the deductible amount cannot exceed net income from the trade or business in which the tips were earned. If your tipping-based business had a low-income year, your deduction is capped at that net income figure. [1]

A third constraint applies to certain service businesses: if you operate a Specified Service Trade or Business (SSTB) under Section 199A, including most consulting, health, law, and financial services practices, CPA analysis concludes you are not eligible for the tips deduction at all. [4]

Service charges and mandatory gratuities are also excluded. The deduction covers voluntary tips, not amounts added automatically to a bill. [4]

If you work in food service, hospitality, or a qualifying salon occupation as a self-employed person, this provision applies to you. If you freelance in design, software, consulting, or healthcare, it does not.

The breaks that do reach Schedule C filers: QBI permanence and the 1099-K rollback

Verdict: For you

These two provisions get less headline attention than tips and overtime. They are more meaningful for most freelancers.

QBI deduction, made permanent. The Section 199A qualified business income deduction was scheduled to expire after 2025. The OBBBA made it permanent. For tax year 2026 and beyond, Schedule C filers can deduct 20% of their net qualified business income. [8]

Some coverage of the OBBBA stated the rate rose to 23%. That figure came from an earlier House version of the bill. It was not enacted. The rate is 20%, and the enacted law kept it there. [8]

For a freelancer with $60,000 in net QBI, that is a $12,000 deduction per year that no longer carries an expiration date. Before the OBBBA, every year of business planning had to account for the possibility that this deduction would disappear. It is now part of the permanent tax code.

For the full QBI calculation, Form 8995 walkthrough, and everything the OBBBA changed and did not change for the deduction, see the QBI Deduction for Self-Employed Filers (2026 Guide).

1099-K threshold rollback. Third-party settlement organizations (PayPal, Venmo, Stripe, and similar platforms) are no longer required to file Form 1099-K unless gross payments exceed $20,000 and more than 200 transactions occur in the year. [5] This reverts the threshold back from the near-$600 rule that had been creating widespread confusion and compliance overhead for freelancers.

Your income is still taxable regardless of whether you receive a 1099-K. What the rollback reduces is the volume of forms, and the risk of receiving a 1099-K that does not match your own records.

The car loan interest deduction and the senior bonus: what to know

Verdict: Conditional

Two more OBBBA provisions appear in some self-employed coverage. Neither is the primary story for most freelancers, but both are worth understanding.

Car loan interest deduction. New for 2026: up to $10,000 in interest on a loan for a new personal-use vehicle, where the original use starts with you and final assembly was in the United States. MAGI phaseout above $100,000 single ($200,000 joint). [6]

For freelancers who already deduct vehicle expenses using the mileage method or actual costs, this interacts with your existing deductions. Any business-use interest you have already claimed reduces what you can take here. CPA analysis notes that for most self-employed taxpayers with business vehicle use, the existing business-vehicle deduction is generally more advantageous than this new personal deduction, and the net benefit of the new provision may be small or zero. [7] Worth reviewing with a tax professional if you carry a car loan and claim a business vehicle deduction.

Senior bonus deduction. A $6,000 additional deduction for filers age 65 or older, with a phaseout above $75,000 single ($150,000 joint). [6] Straightforward if you qualify by age. Neither provision requires Schedule C income; both apply at the individual return level.

Whichever break applies, it starts with your Schedule C number

Every OBBBA provision that reaches Schedule C filers runs through the same foundation. The QBI deduction is 20% of net business income. The tips deduction is capped at net income from the tips-based business. The car loan interest deduction interacts with business-vehicle interest already claimed.

All of these start with your Schedule C net income figure.

That figure is only as defensible as the business expense records behind it. A deduction you cannot substantiate is a deduction that gets disallowed, which raises the profit figure, which raises your QBI, which raises your tax bill. A well-documented home office deduction reduces the Schedule C net income those calculations start from.

The IRS receipt documentation standards that apply to your Schedule C deductions are the same standards that determine the number your OBBBA breaks are calculated from.

TL;DR summary

| OBBBA break | Who it covers | Freelancer verdict | Key condition |

|---|---|---|---|

| No tax on overtime | Employees with FLSA wage-statement overtime | Not for freelancers | No wage statement or FLSA overtime for self-employed |

| No tax on tips | Qualifying tipped occupations | Conditional | Must be on IRS's finalized 70+ occupation list; net-income cap applies |

| QBI permanence | Pass-through business owners | For you | 20% of net QBI; rate did not change to 23% |

| 1099-K rollback | Gig-payment recipients | For you | Threshold reverts to $20,000 / 200 transactions |

| Car loan interest | New personal-vehicle borrowers | Conditional | Reduced by any business-use vehicle interest already claimed |

The 2026 tax breaks for freelancers that actually move your bill are the permanence of a deduction that has been in the tax code since 2018 and a paperwork threshold that stopped making sense at $600. The provisions that generated the most excitement mostly describe employee income. Plan your estimates around what is actually in the law.

These are federal rules as published by the IRS and reflected in independent CPA and tax analysis. This is general information, not tax advice. Your specific situation may involve factors that change how the rules apply to you. A tax professional can work through that.

References

- IRS, "One, Big, Beautiful Bill: How to take advantage of no tax on tips and overtime" https://www.irs.gov/newsroom/one-big-beautiful-bill-how-to-take-advantage-of-no-tax-on-tips-and-overtime

- IRS, "What to know about the No Tax on Overtime deduction" https://www.irs.gov/newsroom/what-to-know-about-the-no-tax-on-overtime-deduction

- IRS, "Treasury, IRS issue final regulations listing occupations where workers customarily and regularly receive tips under the One, Big, Beautiful Bill" https://www.irs.gov/newsroom/treasury-irs-issue-final-regulations-listing-occupations-where-workers-customarily-and-regularly-receive-tips-under-the-one-big-beautiful-bill

- RSM US, "No tax on tips: Final rules confirm qualifying occupations and tip definition" https://rsmus.com/insights/tax-alerts/2026/no-tax-tips-final-rules-confirm-qualifying-occupations-tip-definition.html

- IRS, "IRS issues FAQs on Form 1099-K threshold under the One, Big, Beautiful Bill; dollar limit reverts to $20,000" https://www.irs.gov/newsroom/irs-issues-faqs-on-form-1099-k-threshold-under-the-one-big-beautiful-bill-dollar-limit-reverts-to-20000

- IRS, "One, Big, Beautiful Bill Act: Tax deductions for working Americans and seniors" https://www.irs.gov/newsroom/one-big-beautiful-bill-act-tax-deductions-for-working-americans-and-seniors

- RSM US, "Understanding the OBBBA car loan interest deduction" https://rsmus.com/insights/services/business-tax/understanding-obbba-car-loan-interest-deduction.html

- Tax Foundation, "199A Deduction: Pass-Through Business Deduction and the Big Beautiful Bill" https://taxfoundation.org/blog/199a-deduction-pass-through-business-big-beautiful-bill/