What Disorganized Receipts Are Actually Costing You (It's Not Just the Missed Deductions)

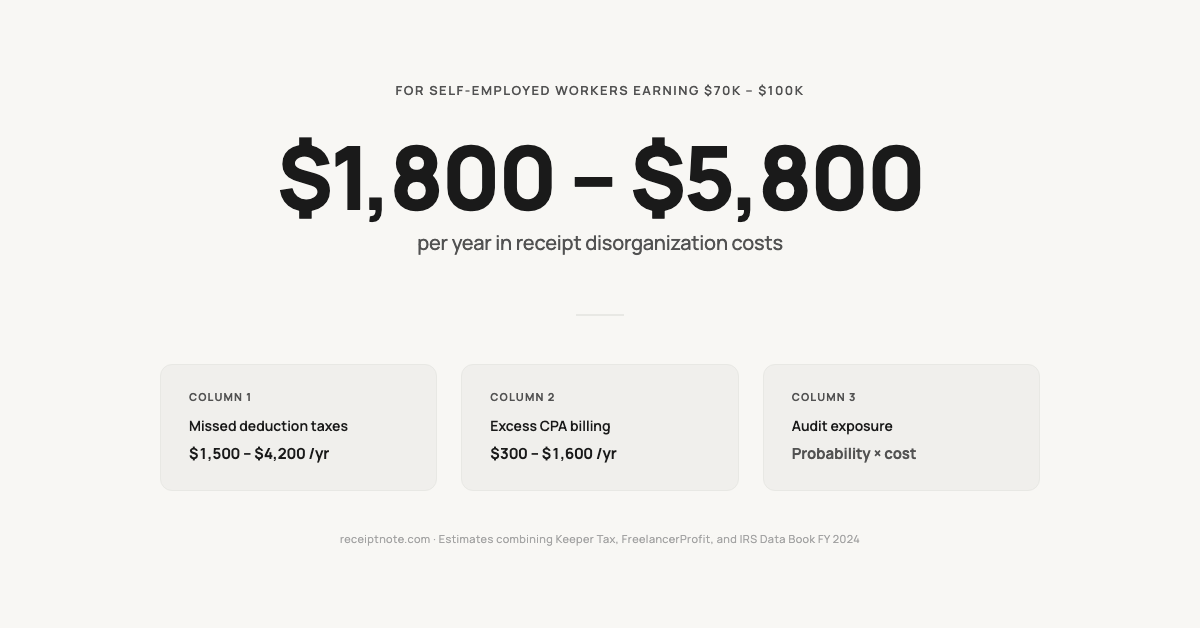

Most freelancers estimate their receipt chaos costs a few hundred dollars in missed deductions. The honest number runs in three columns: missed deduction taxes, excess accountant billing, and audit exposure. For a self-employed person earning $70K to $100K, the full stack is closer to $1,800 to $5,800 a year. Here is the math.

For a self-employed earner at $70K to $100K, the honest stack of receipt disorganization costs runs $1,800 to $5,800 per year across three simultaneous columns.

Most self-employed people have already made peace with their receipt habit. They know it is not great. They also carry a rough number for what disorganized receipts cost them: a few hundred dollars in missed deductions, the price of being a little disorganized. Annoying, but manageable.

That number is wrong, and not by a little.

A Keeper analysis of 205 gig-worker tax returns, reviewed by an IRS Enrolled Agent, found the average 1099 contractor overpays taxes by about 21 percent. [1] At $25,000 in contracting income, that is roughly $1,550 a year. And that figure measures only one thing: deductions left on the table. It does not count what disorganized records cost you at the accountant's desk, or what they expose you to if your return is ever examined.

The cost of receipt disorganization runs in three columns at once. Most freelancers add up only the first one. This post adds up all three, so you can decide whether your current system is worth what you are actually paying for it. For a self-employed person earning $70,000 to $100,000, the honest stack lands somewhere between $1,800 and $5,800 a year.

Start with the column you already know. It is larger than most people count.

The three-column cost, at a glance>

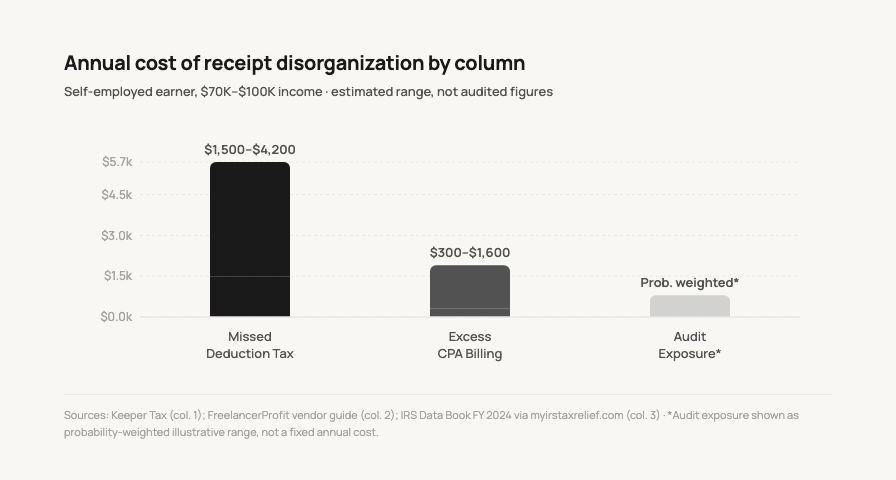

- Missed deduction taxes: about $1,500 to $4,200 a year

- Excess accountant billing: about $300 to $1,600 a year

- Audit exposure: a probability, not a fixed line item, but not zero>

Composite estimate for a $70K to $100K earner: roughly $1,800 to $5,800 a year. These figures combine sources with different methods and are estimates, not an audited calculation. The sourcing notes throughout say which is which.

What disorganized receipts cost in missed deductions

The common mistake is to count this column in expense dollars. You think, "I probably missed maybe a thousand dollars of write-offs." But a missed write-off does not cost you a thousand dollars. It costs you the tax on it. The right unit is overpaid tax, and that is what makes the Keeper number land: 21 percent overpaid, on average, by people whose income is mostly 1099. [1]

Look at what actually goes missing. In the same Keeper analysis, the most commonly overlooked deductions were not exotic. Phone bills were missed by 23 percent of gig workers, software subscriptions by 21 percent, car insurance and roadside coverage by 19 percent, business meals by 16 percent. [1] These are the ordinary running costs of self-employment. They go undeducted not because the rules are obscure but because the receipt was never captured, or was captured and never categorized.

The dollar size depends on income. A vendor guide from FreelancerProfit walks through a digital marketing consultant earning $95,000 with $14,000 in undocumented expenses, and puts the missed deduction tax at about $4,200, using an effective rate near 30 percent once federal income tax, self-employment tax, and state tax are stacked. [2] (That is a vendor-produced example, not an independent study. Treat it as illustration, not benchmark.) At the other end, a more conservative vendor scenario from Neat assumes $200 a month in untracked deductible spend, which works out to $2,400 a year in expenses and about $600 in extra tax at a 25 percent rate. [3]

So the deduction column alone spans roughly $600 to $4,200. That spread is not a menu to pick a comfortable number from. It tracks your income, your expense volume, and how many of those most-missed categories apply to you. A freelancer at $70,000 with a phone plan, a few monthly software subscriptions, and a home office sits well above the floor, not at it.

One objection belongs here, briefly: "My accountant catches what I miss." An accountant can only work from what exists. A phone bill with no record of business use does not become a 60 percent business deduction on its own. Someone has to decide and document the split. That work is the second column.

What your accountant charges to organize the mess

This is the column almost no consumer guide mentions, and it is the one that shows up first, before the return is even filed.

When records arrive disorganized, the accountant does not start by filing. They start by organizing: matching charges to categories, chasing the receipts you forgot to send, asking what a $340 charge to a vendor they have never heard of was for. FreelancerProfit estimates CPA hourly rates of $150 to $400 and 2 to 4 extra billable hours a year spent on that cleanup for a disorganized client, which comes to roughly $300 to $1,600 in extra billing. [2] Again, vendor figures, so hold them as a range rather than a quote. But the direction is not controversial. Time spent sorting your shoebox is time you pay for at a professional rate.

Be precise about what your accountant can and cannot do for you. They can apply the rules expertly. They cannot manufacture a record that was never made. A restaurant receipt that reads "Café Luna, $85" with nothing written about who you met or why is not a documented business meal. It is a charge. Turning it into a deduction requires the business purpose, and a careful preparer will not invent one on a return they sign. As one accountant, Racheal Layton, put it in a WorkLife interview, "One missed receipt could make a huge impact on the tax return." [4]

Notice what this column does not require. No audit. No bad luck. The cleanup bill arrives every year, on the invoice, regardless of whether anything ever goes wrong. Two columns so far, and neither depends on an unlikely event.

The third one does. It hinges on something that probably will not happen. The instinct is to file it under "audit fear" and move on. That instinct skips the arithmetic.

Audit exposure, counted as probability times cost

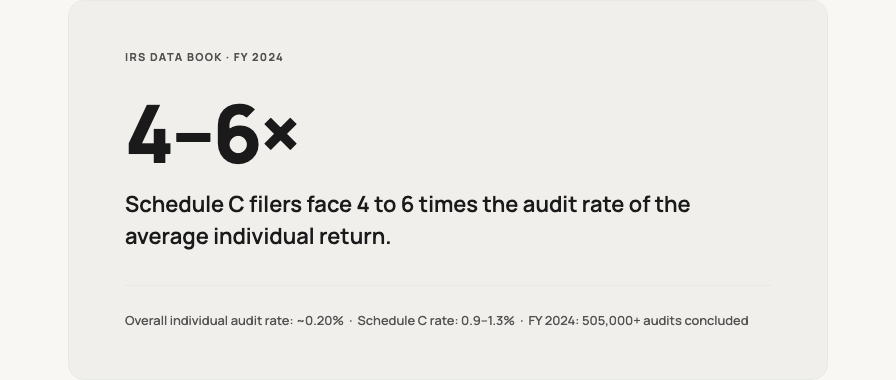

Here are the numbers, from the IRS Data Book for fiscal year 2024 as compiled by a tax-relief practice. The overall individual audit rate is about 0.20 percent, roughly two returns in a thousand. For returns with a Schedule C, the business form sole proprietors file, the rate runs 0.9 to 1.3 percent. [5] That is four to six times the baseline. In FY 2024, the IRS concluded over 505,000 audits and recommended more than $29 billion in additional tax. [5]

Now, 0.9 percent feels like a rounding error, and treated as a standalone probability it almost is. But probability is only half of an expected cost. The other half is the size of the finding if it happens. A self-employed person at $80,000 with $14,000 in undocumented expenses is precisely the profile the IRS scoring system, the Discriminant Function System, treats as above baseline: high deductions relative to income, thin documentation. The expected cost is not zero. It is a small chance of a finding that is not small.

This is where the most reasonable-sounding objection comes in: "I can reconstruct everything from my bank statements in March." Sometimes you can. A clean card charge with an obvious business purpose reconstructs fine. What does not reconstruct: cash payments, expenses run through a mixed personal-and-business account, the business-use percentage on a phone or a car, and the business purpose on a meal. IRS Publication 463 is explicit that records made at or near the time of an expense carry more weight than records reconstructed later. [6] A bank line that says "$85, Café Luna" proves you paid. It does not prove why. (For the specific elements a record has to establish, see What IRS Receipt Requirements Mean for Your Records.)

So three columns, each with a real annual cost. The harder part is not that they add up. It is that they all trace back to the same small failure.

One missing receipt, three simultaneous costs

Walk through a single receipt and watch all three columns move at once.

You take a client to lunch. The bill is $85. The receipt goes into a coat pocket and never makes it into a record. By February it is gone, or faded, or just forgotten. Three things follow from that one slip:

First, the deduction. A documented business meal, with the client's name and the reason for the meeting, is deductible. Missing it at a 30 percent effective rate costs about $25 in extra tax. Once is nothing. A year of forgotten coffees and lunches and the occasional dinner is the deduction column filling up, twenty-five dollars at a time.

Second, the billing. That receipt is one of dozens your accountant has to ask about or set aside. Each undocumented item costs a few minutes of investigate-or-skip. Across a return, those minutes are the billable hours from the second column.

Third, the exposure. If this return is examined and a meal deduction was claimed off a reconstructed statement, the question is simple: what was the business purpose? The contemporaneous note that would have answered it was never written. That is the kind of line that draws a second look.

One receipt. Three costs, from a single missed capture. That is the structure a one-column estimate cannot see, because it is only ever looking at the first column.

A fair word on the numbers in that chart. They come from sources that do not share a method. Keeper is a reviewed analysis of real returns. [1] The IRS audit rates trace to the IRS Data Book. [5] The CPA-billing and named-consultant figures are from a vendor guide. [2] The composite is an estimate built from all of them, not a single audited calculation, and the gap between the low and high end is the honest part: it depends on your income, your records, and your luck. If this changes the math for someone you work alongside, send it to them. The arithmetic is more persuasive than the nagging.

With all three columns visible, "I'll sort it out at tax time" becomes a different decision. Not necessarily the wrong one. But a decision made against the real number instead of a partial one.

Running your own three-column number

You do not need this post's range. You can build your own, and it is more useful because it is yours.

Three questions get you most of the way. What is your rough annual volume of undocumented or untracked deductible spend? What is your effective tax rate once self-employment tax is included? And what does your accountant charge per hour, multiplied by the hours your disorganization adds to the engagement? The first two questions size the deduction column. The third sizes the billing column. The audit column stays a probability you weigh rather than a number you add, which is the honest way to carry it.

For context on the effort side of that trade, FreelancerProfit estimates about 90 minutes a month of maintenance to keep records in the state that avoids the stack in their $6,800 example. [2] Whether 90 minutes a month is worth $1,800 to $5,800 a year is genuinely your call, and it depends on numbers only you have.

If you decide the current system is costing more than it saves, the fix is a routine, not a heroic cleanup. A monthly habit keeps the pile small enough that none of the three columns gets a chance to fill: see A Freelancer's Month-End Receipt Closeout for the 30-minute version, and 5 Receipt Scanning Tips That Save Hours at Tax Time for the capture habit that feeds it. Receipt capture apps handle the capture at the point of spend, where the business purpose is still fresh in your head; ReceiptNote is one option self-employed workers use for that.

The point is not to feel bad about a coat-pocket receipt. It is to know what the coat pocket costs, and then choose on purpose.

References

- Keeper: Gig Workers Overpay on Taxes by 21 Percent (analysis of 205 gig-worker returns with at least $600 in 1099 income, reviewed by an IRS Enrolled Agent; vendor study, not a government figure) https://www.keepertax.com/research/gig-workers-overpay-on-taxes-by-21-percent

- FreelancerProfit: Consistent Accounting Records, 2026 Freelancer Guide (vendor-produced guide; named-consultant example and CPA-billing figures are illustrative, not an audited study) https://freelancerprofit.com/consistent-accounting-records/

- Neat: The True Cost of Staying Disorganized (vendor blog; hypothetical $200/month untracked-spend scenario, not a study) https://www.neat.com/blog/expense-tracking-system-small-business

- WorkLife: How freelancers are losing money due to a complex tax process (interview-based; quote attributed to accountant Racheal Layton) https://www.worklife.news/talent/tax-season-freelancers/

- My IRS Tax Relief: IRS Tax Audit Statistics and Overview, updated 2024 data (compiles IRS Data Book FY 2024 figures: 0.20% overall individual audit rate, 0.9 to 1.3% Schedule C rate, 505,000+ audits, $29B+ additional tax recommended) https://www.myirstaxrelief.com/back-tax-help/irs-tax-help/irs-tax-audit-statistics-overview/

- IRS Publication 463: Travel, Gift, and Car Expenses (recordkeeping standard; records made at or near the time of an expense carry more weight than reconstructed records) https://www.irs.gov/publications/p463